Should You Buy Established or New Property in Australia?

Seven factors to compare before making an investment decision

When it comes to building a successful property portfolio in Australia, one question comes up again and again: Should I invest in an established property or a brand-new one? It’s a choice that can shape your financial future, yet many buyers are influenced by marketing rather than facts. Ads promoting rental guarantees, tax depreciation benefits, or “growth corridors” can make new properties seem like the obvious pick. But are they really the better option?

The reality is, there’s no one-size-fits-all answer. Understanding the trade-offs between old and new properties is essential before you commit hundreds of thousands of dollars. That’s where a buyer's agent can help. A qualified buyer's agent works for you — not the developer or seller — and can guide you through key decisions by using independent data, local expertise, and market knowledge.

In this article, we’ll break down the key differences between established and new properties across seven categories that matter most to investors:

Capital growth

Depreciation and tax

Tenant appeal

Maintenance

Value-adding potential

Land-to-asset ratio

Developer incentives

Whether you’re a first-time buyer or planning your next investment, this comparison can help you avoid costly mistakes and make a more informed decision. We’ll also explain how BuyerAgentFinder helps you find the right agent to support your strategy and maximise your outcomes.

1. Capital Growth

When you’re buying an investment property, long-term capital growth is one of the most important outcomes to aim for. Many investors ask: Should I buy an established property for growth? In most cases, the answer leans towards yes, and the reason comes down to supply and demand.

New properties are often built on the outer edges of cities where land is plentiful. These areas are filled with house-and-land packages, townhouses, and off-the-plan developments. Because there’s so much land available, developers can continue to release new stock year after year. That constant supply limits the potential for strong price growth.

Established homes, on the other hand, are typically located in inner or middle-ring suburbs where land is scarce. These suburbs are already developed, with limited space for new builds. Scarcity drives demand, and that’s what puts upward pressure on prices over time.

Another key point is the land-to-asset ratio. In established homes, a greater proportion of the purchase price is tied to the land itself, which is the part that increases in value. Buildings, by contrast, depreciate over time. If you’re paying $700,000 for a brand-new townhouse where most of the value is in the building, you’re not setting yourself up for strong capital growth.

In summary:

More supply = less growth in new estates

Scarcity = more growth in established areas

Land grows in value, buildings lose value

If your goal is to build equity and grow your portfolio, it’s worth prioritising properties where the majority of the value is in the land, not the building. A local buyers' agent can help you identify suburbs and properties where capital growth potential is strongest, based on independent data and historical performance.

Depreciation & Tax Strategy

A major selling point often used to promote brand-new properties is the tax benefit of depreciation. The idea is simple: the newer the property, the more you can claim as a deduction on your tax return. But this is where many investors get caught out, assuming depreciation is “free money” and choosing a property based on this benefit alone.

The Depreciation Trap

New properties do offer higher depreciation in the short term, especially on the building structure and fixtures. However, when the time comes to sell, you’ll be required to pay back a portion of that benefit to the ATO. This is known as a depreciation claw-back, and it can reduce your final profit significantly.

For example, if you’ve claimed $100,000 in depreciation over a 10-year period, you could be handing back around $45,000 when you sell. That’s a large tax bill that often surprises first-time investors who weren’t aware of this catch.

Depreciation in Established Homes

Many people believe that established properties offer no depreciation at all. That’s not accurate. While the depreciation on the building may be lower or already claimed by a previous owner, you can still benefit from deductions on:

Renovations or structural improvements (depending on when they were completed)

Plant and equipment items, if the property was recently updated

Professional depreciation schedules prepared by a quantity surveyor

In other words, investment property depreciation in Australia is still available on older homes; you just need to be smarter about it. And because established homes often come with more land value and better capital growth, the overall investment outcome can be far more favourable, even if the depreciation benefits aren’t as high upfront.

If your goal is to reduce tax while still growing long-term wealth, depreciation should be seen as a bonus, not the main reason to buy. A qualified buyer's agent can help you weigh these factors and avoid being swayed by short-term tax incentives alone.

Rental Demand & Tenant Appeal

One of the main reasons investors choose brand-new homes is the belief that new builds will attract better tenants and command higher rents. On the surface, this sounds logical: modern finishes, new appliances, and freshly built homes seem like easy rentals. But what’s often overlooked is how location and supply affect rental demand.

Oversupply in New Estates

Fringe suburbs with new estates can look appealing in developer brochures. However, these areas are often packed with house-and-land packages being marketed to investors at the same time. In many of these neighbourhoods, a high percentage of homes are owned by landlords, not owner-occupiers.

This creates a situation where there are too many similar properties competing for the same pool of tenants. When vacancies rise, rents stagnate or fall. Promises of a “rental guarantee” might offer short-term comfort, but these guarantees are typically built into the purchase price and expire within a few years. Once that guarantee ends, the property will only earn what the open market is willing to pay.

Stability in Established Suburbs

In contrast, established suburbs tend to have a mix of owner-occupiers and long-term renters. These areas often have:

Existing infrastructure (schools, shops, transport)

Community demand

Lower vacancy rates

More consistent rental growth

Tenants looking for proximity to the CBD, public transport, or good schools tend to favour these locations. That means fewer vacancy periods and a stronger base for rent increases over time.

How a Property Buyer's Agent Can Help

A property buyer's agent with local experience can guide you toward areas with strong rental demand and low vacancy rates. Rather than relying on marketing brochures or developer promises, a buyer's agent looks at actual rental performance, population trends, and tenant preferences to recommend investment-grade suburbs.

Maintenance Costs

Maintenance is one of the most common concerns for property investors, especially those considering older homes. It’s true that new builds generally come with fewer repair issues in the early years. But choosing a property purely to avoid maintenance costs can lead to missed opportunities for capital growth.

New vs Old: Cost Comparison

Let’s look at a basic example.

A new property might cost around $500 per year in maintenance for the first 5 to 7 years.

An established property, depending on age and condition, might average around $2,000 per year.

Over 10 years, that’s a $15,000 difference.

While that might sound significant at first, it’s small compared to what you could be giving up in capital gains. Properties in established suburbs, where land is scarce and demand is higher, tend to outperform newer estates in long-term value growth. Sacrificing capital growth to save on repairs could cost you hundreds of thousands of dollars in missed equity over time.

Why This Matters for Investors

Many investors are told to buy new to “avoid the hassle.” But saving a few thousand dollars on repairs isn’t worth it if the property doesn’t grow in value. An experienced buyer's agent will help you assess the true cost of ownership, including maintenance against expected growth, rental income, and long-term goals.

Renovation & Value‑Add Opportunities

One of the biggest advantages of buying an established property is the potential to add value through renovation. Whether it’s a cosmetic update or a structural improvement, smart upgrades can boost equity and increase rental income, giving you more options to grow your portfolio.

Equity Uplift from Renovations

With the right strategy, a well-located older home can be improved for a relatively low cost, delivering significant returns. For example:

Spend $20,000 on a kitchen and bathroom refresh

Increase the property’s value by $60,000–$80,000

Revalue and use the equity to fund your next deposit

This “value-add” approach helps investors accelerate their portfolio growth without relying solely on market movement. Renovations can also improve tenant appeal, shorten vacancy periods, and justify rent increases.

Why New Builds Offer Less Flexibility

By contrast, new properties leave little room for improvement. There’s nothing to renovate, and councils often restrict redevelopment or changes in new estates. You’re buying the property at its full market value with all the features already priced in, so the only growth you can expect is from the market itself.

If you’re looking to grow faster, older properties offer more control and flexibility. They allow you to manufacture equity, add rental appeal, and take an active role in your investment journey.

A property buyer's agent can help you find properties with strong renovation potential, whether it’s a freestanding home in a growth suburb or a unit with scope to add value.

Land-to-Asset Ratio

A key concept that often separates high-performing properties from underperforming ones is the land-to-asset ratio. This simple but powerful idea refers to how much of the property’s total value is tied to the land versus the building.

Why the Land Component Matters

In Australian property markets, land is what grows in value over time. The building itself depreciates, both physically and from a tax perspective. That’s why properties with a higher proportion of their value in the land—rather than in the structure—tend to see better capital growth over the long term.

Here’s a comparison:

A brand-new townhouse in a new estate might sell for $750,000, but only $250,000 of that is land. The rest is in the building, which depreciates.

An older home in a growth suburb might also cost $750,000, but $500,000 of that value could be land. This puts the investor in a stronger position for future equity gains.

A higher land-to-asset ratio generally means:

Greater long-term appreciation

More stable asset value during market corrections

Better borrowing power as equity grows

Connecting the Dots with Capital Growth

If you’re asking yourself whether a property will help you build wealth over time, look closely at the land value. Areas where land is limited and in demand, such as inner and middle-ring suburbs, offer better protection against oversupply and better chances of growth.

A buyer's agent can help you assess land-to-asset ratios and target properties with the right balance. They understand how to spot undervalued land in well-performing suburbs and can guide you towards smarter long-term investments.

Developer & Vendor Incentives

One of the least understood risks in new property investment is the conflict of interest built into the way many developments are marketed. What looks like helpful advice from a property consultant or buyers' agent may actually be a sales pitch in disguise, driven by incentives paid by developers.

Who Is Really Representing You?

In many cases, developers rely on a network of marketers, spruikers, and so-called “property advisors” to sell their new stock. These intermediaries are often paid tens of thousands of dollars in commissions per sale. While they may present themselves as acting in your best interests, they are actually working for the vendor or developer, not for you.

This is especially common in house-and-land packages, off-the-plan apartments, and large new estates. These companies may offer a “free service” or include education as part of their pitch, but the real goal is to sell specific properties once they’re financially incentivised to move.

The Truth About Rental Guarantees and Depreciation

Two common tactics used in these pitches are rental guarantees and depreciation benefits.

Rental guarantees might sound reassuring, but they’re often built into the purchase price. That means you’ve already paid for the guarantee upfront, and once it ends, typically after a few years, you’re left with a property that must compete in the open rental market. If the area is oversupplied, rents may fall well below what was originally promised.

Depreciation benefits, especially on brand-new properties, are heavily promoted to make the investment seem more attractive from a cash flow perspective. While it’s true that new properties come with higher depreciation deductions, many investors are not told that a large portion of these deductions must be paid back to the ATO when the property is sold. This “claw-back” can significantly reduce your overall return.

Work With Someone Who Works for You

The best way to avoid being caught out by incentives and marketing hype is to work with a qualified property buyer's agent, someone who represents you, not the vendor. A buyer's agent can assess the property on its real investment potential, including growth prospects, rental demand, and financial performance, without bias.

Through BuyerAgentFinder.com.au, you can compare independent buyers' agents who don’t take commissions from developers and who are focused on helping you make better decisions based on your goals, not someone else’s sales target.

How a Buyer's Agent Helps You Decide

Choosing between a new or established investment property isn’t just about features and finishes; it’s about long-term performance, rental demand, and what suits your goals. This is where working with a buyer's agent near me can make all the difference.

A local buyer's agent brings independent advice, suburb expertise, and detailed research into the picture. They’re not influenced by developer commissions or vendor incentives. Their role is to guide you through the options and help you buy a property that aligns with your budget, risk profile, and investment timeline.

At BuyerAgentFinder, we make this process easier. Our platform lets you:

Compare pre-screened, licensed buyer's agents across Australia

Filter by suburb, experience, and property type

Read verified reviews and track record summaries

Request a free 45‑minute consultation with agents who match your needs

Rather than searching endlessly for the “right” buyer's agent near me, you can let the system do the hard work. Whether you’re leaning toward an established house or considering a newer build, an experienced agent will help you weigh the trade-offs without sales pressure.

Click here to book your free 45‑minute session and connect with buyer's agents who act only in your best interest.

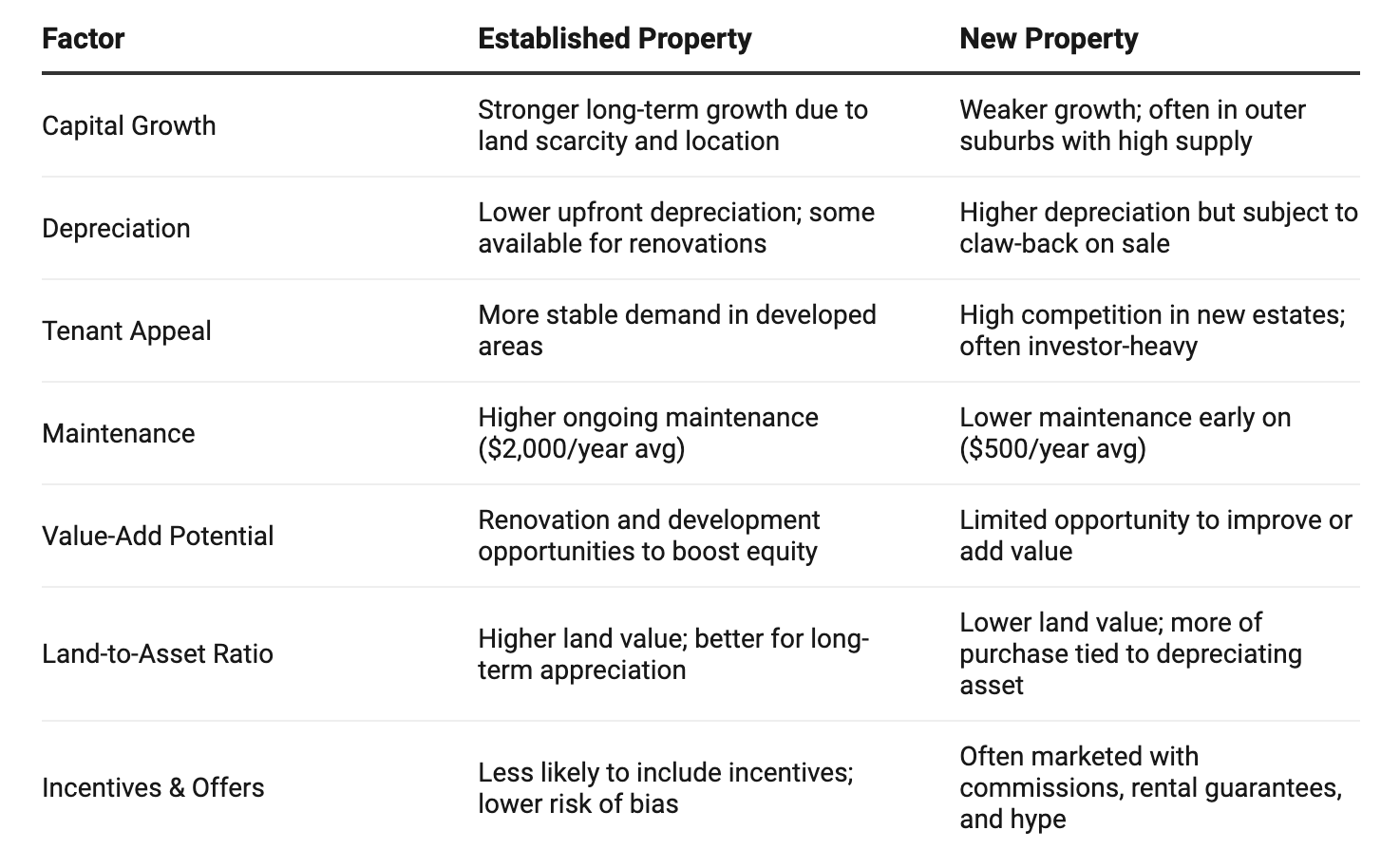

Summary Table: Pros & Cons Side‑By‑Side

Here’s a quick comparison of new vs established properties across the seven key factors discussed. Use this as a reference when deciding what suits your investment goals.

Conclusion

When deciding whether to invest in a new or established property, it’s essential to look beyond marketing promises and weigh the facts. Throughout this article, we’ve compared both options across seven critical factors:

Capital growth: established homes tend to outperform due to scarcity and location

Depreciation: new builds offer upfront benefits, but come with future tax claw-back

Tenant appeal: older suburbs often attract more stable demand and lower vacancies

Maintenance: newer homes are cheaper to maintain, but growth is often weaker

Value-add potential: renovations can unlock equity in older homes

Land-to-asset ratio: land appreciates, buildings don’t — older homes usually offer better ratios

Incentives: rental guarantees and depreciation benefits often benefit the seller more than the buyer

If you’re still unsure which direction to take, speaking with a buyer's agent can help clarify your options. They can guide you based on actual data, your investment goals, and what’s performing in your target suburbs.

Use BuyerAgentFinder.com.au to:

Search for a buyer's agent near you

Compare suburb specialists

Book a free 45‑minute consultation to discuss your goals

Don’t let commissions or marketing hype influence your biggest financial decisions. Get advice that’s on your side and make smarter investment moves with the right support.

Sponsored by BuyerAgentFinder

Partner with Us

Promote your business to over 14,000 engaged property buyers and investors across Australia through the Australian Property Market blog and newsletter.

If you’re a brand aligned with real estate, finance, development, or property services, we’d love to explore sponsorship opportunities with you.

Email: mehran5454 at yahoo.com to enquire about partnerships.